When working with time series data, it’s common to deal with daily or irregular data and then convert it into more manageable chunks like monthly or yearly aggregates.

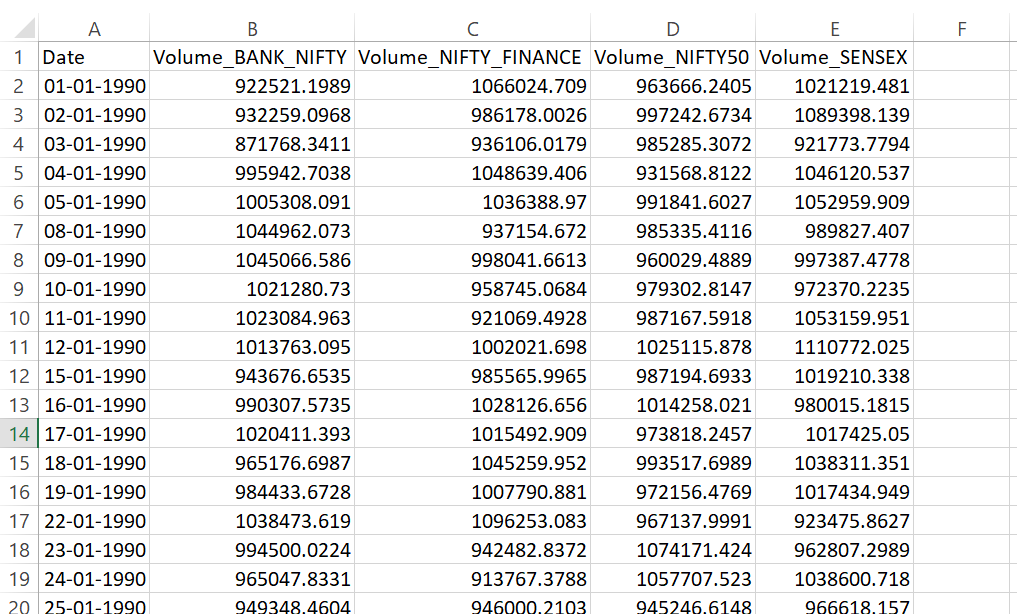

Below is a snapshot of daily trading volumes for stock indices Bank Nifty, Nifty Finance, Nifty 50, and Sensex.

import pandas as pd

# Load the CSV

df = pd.read_csv("daily_data.csv", parse_dates=["Date"], index_col="Date")

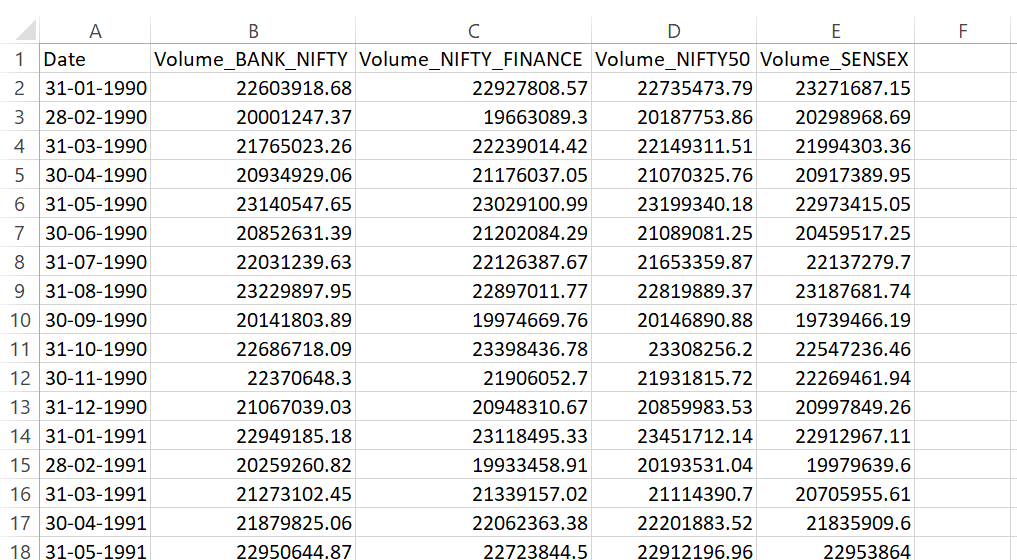

# Covert to monthly and sum the other cols

monthly_data = df.resample('M').sum()

print(monthly_data.head())

You can extend this analysis to calculate monthly averages, medians, or other aggregations. For example, mean, median, or maximum monthly trading volumes can be calculated.

import pandas as pd

# Load the CSV

df = pd.read_csv("daily_data.csv", parse_dates=["Date"], index_col="Date")

# Monthly average

monthly_avg = df.resample('M').mean()

print("Monthly Average Volumes:")

print(monthly_avg.head())

# Monthly median

monthly_median = df.resample('M').median()

print("\nMonthly Median Volumes:")

print(monthly_median.head())

# Monthly maximum

monthly_max = df.resample('M').max()

print("\nMonthly Maximum Volumes:")

print(monthly_max.head())